Published by Finnex | Federal Budget Series

Property investors and anyone holding assets – shares, crypto, managed funds or business assets – need to pay close attention to the 2026 Federal Budget.

Property Investor Tax Changes: Two significant reforms have been announced: changes to negative gearing for residential investment properties, and changes to the capital gains tax (CGT) discount. Neither applies immediately, but both require investors to think carefully about strategy, timing and their next move.

Here’s a clear breakdown of what’s changing, when it applies, and what to consider before you sign any contracts.

Property Investor Tax Changes: Negative Gearing – What’s Changing from 1 July 2027

Currently, if a rental property produces a tax loss – because rental expenses exceed rental income – many investors can use that loss to reduce other taxable income, such as salary and wages. This is negative gearing.

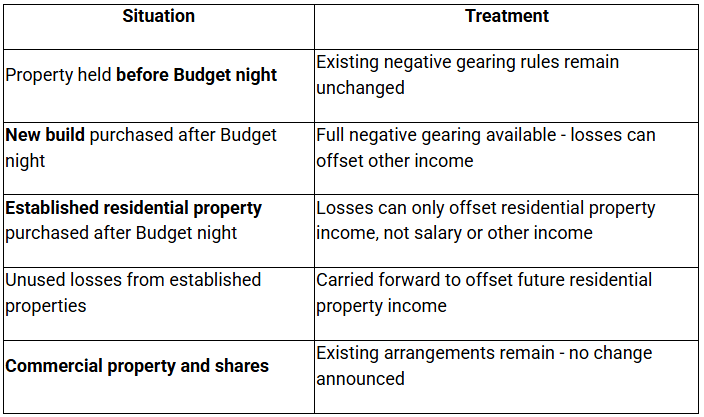

From 1 July 2027, the Government proposes to limit negative gearing for residential investment properties to new builds.

Here’s how the transitional rules are expected to work:

Negative gearing is not disappearing entirely. For new builds and existing holdings, it remains a valid tax strategy. But for investors buying established residential properties after Budget night, the rules are materially different.

What this means before you sign a contract

If your investment strategy relies on negative gearing against salary or other income, the distinction between a new build and an established property has become one of the most important decisions you’ll make.

Before committing to a purchase, understand:

- Whether the property is a new build or an established one

- When the contract is entered into relative to the Budget night

- Whether the property can still be negatively geared against your other income

- How will losses be treated if they cannot offset other income

- Whether the investment makes commercial sense without the same tax benefit

A property should never be purchased purely for the tax deduction – particularly when the rules are in the process of changing.

Capital Gains Tax – A Major Structural Change

Property Investor Tax Changes: The Budget also proposes significant changes to how capital gains are taxed from 1 July 2027.

Currently, individuals, trusts and some partnerships may be eligible for a 50% CGT discount on assets held for at least 12 months – meaning only half the capital gain is included in assessable income.

From 1 July 2027, the Government proposes to:

- Replace the 50% CGT discount with cost base indexation – adjusting the cost base of the asset for inflation before calculating the gain

- Introduce a 30% minimum tax rate on real capital gains accruing after 1 July 2027

This is a structural shift. Instead of discounting the gain by half, the new system focuses on the real gain after inflation is removed – and then taxes that real gain at a minimum rate of 30%.

Key points for investors:

- The changes apply to gains accruing from 1 July 2027. Gains accrued before that date are expected to be treated under current rules

- This affects more than just property – shares, crypto, managed fund investments, business assets and inherited assets may all be caught

- Investors in new builds may be able to choose between the 50% CGT discount and the new indexation rules

- The main residence exemption remains a separate rule. Selling your primary home may still be fully or partly exempt from CGT, depending on your circumstances

What this could mean in practice

Whether indexation produces a better or worse result than the 50% discount depends on:

- How long have you held the asset

- The inflation rate over the holding period

- Your marginal tax rate

- The size of the gain

For assets held over very long periods in a high-inflation environment, indexation may produce a competitive result. For shorter holding periods or assets with very large gains, the outcome may differ significantly.

Before you sell: If you’re considering selling an investment property, shares or other assets, the timing of the sale relative to 1 July 2027 may have a material tax impact. That decision shouldn’t be made on tax alone – but the tax outcome should absolutely be reviewed before contracts are exchanged.

Planning Checklist for Investors

Use this as a starting point – not a replacement for advice specific to your situation:

- If you hold investment properties purchased before Budget night, confirm your transitional position

- If you’re considering purchasing a residential investment property, determine whether it qualifies as a new build

- If you hold assets with large unrealised gains (property, shares, crypto), review the timing implications before any disposal

- If you hold assets across a trust or partnership structure, seek specific advice on how the CGT changes may apply

- Review whether your investment strategy still makes sense under the proposed new rules

The Bottom Line

Property Investor Tax Changes: The 2026 Budget does not dismantle negative gearing or CGT concessions – but it significantly reshapes them for future acquisitions and future gains. The rules for existing holdings and new builds look very different from those applying to established property purchases and long-term asset disposals after 2027.

Timing, asset type and structure all matter more than they did before.

Are you an employee or individual taxpayer also affected by this Budget? Read our employee and individual guide here: 2026 Federal Budget: What Every Employee Needs to Know

ABN holder or sole trader? Some of these Budget changes may also intersect with your business income. Read more: 2026 Federal Budget: What ABN Holders and Sole Traders Need to Know

Tax NextGen’s registered tax agents can help you model the impact of these changes on your specific portfolio and tax position. Don’t make property or investment decisions before understanding the full tax picture. Book a tax consultation today.